In 2022, the Australia beef industry is set to continue its herd rebuilding phase which began in 2021. As the herd numbers have begun to recover, overall cattle slaughter is expected to rise from the 50-year low of last year. With ample pasture production in key beef producing areas, and a continued high proportion of cattle finished by feedlots, carcass weights are expected to improve moderately in 2022.

Higher slaughter and strong slaughter weights are expected to result in a 12 percent rise in beef production and a 13 percent increase in beef exports for 2022. For pork, another record grain harvest has helped curtail any increase in feed costs, and this combined with strong pork prices are expected to result in Australia’s 2022 pork production matching last year’s record level.

EXECUTIVE SUMMARY

In 2022 the Australia beef industry is set to continue its herd rebuilding phase which began in 2021. As the herd numbers have begun to recover, overall cattle slaughter is expected to rise from the 50-year low of last year.

In the south-eastern states, particularly New South Wales, since early 2020 rainfall and pasture production has been excellent, and these areas have led the way in terms of the herd recovery. Northern parts of Queensland and the Northern Territory have also received increases in rainfall but these have not been to the extent experienced in more southern regions across 2020 and 2021. As a result, these

regions are a little less advanced in their herd rebuilding phase compared to the rest of the beef cattle producing regions.

With ample pasture production in key beef producing areas, and a continued high proportion of cattle finished by feedlots, carcass weights are expected to improve marginally in 2022. Higher slaughter and strong slaughter weights are expected to result in a 12 percent rise in beef production and a 13 percent increase in beef exports for 2022. For pork, another record grain harvest has helped curtail any increase in feed costs, and this combined with strong pork prices are expected to result in Australia’s 2022 pork production matching last year’s record level.

CATTLE Production 2022

Cattle (calf crop) production in 2022 is forecast to increase by seven percent from the prior year. This higher cattle production is due to a shift towards increasing beef cow breeding stock that started in 2020 after many cattle producing regions received much improved pasture production conditions. This pasture improvement started in 2020, and this has flowed through all of 2021 and into early 2022.

The increased retention of female calves in 2020 as breeders, many of which will be first calf heifers in 2022, will filter through to supporting an increased calf crop in 2022. This is expected to be a key turning point in starting to rebuild the breeding herd and it is anticipated that there will be a further increased rate of the calf crop in 2023.

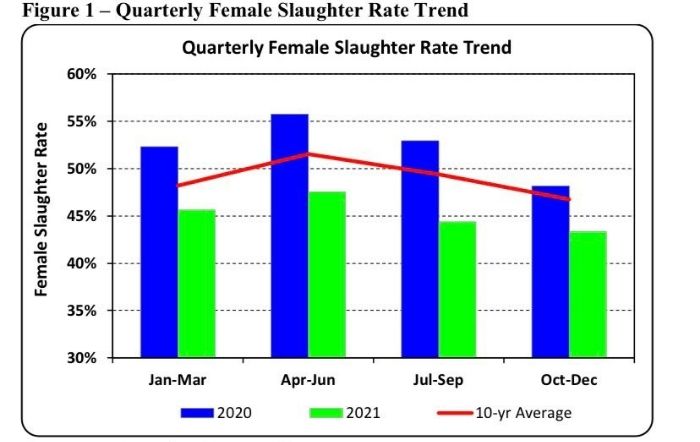

An additional contributor to the increasing calf crop is that the female slaughter rate in 2022 is expected to remain low at 45 percent and similar to the rates in 2021. These rates are well below the previous 10- year annual average female slaughter rate of 49 percent. They are also well below the broadly accepted rate of 47 percent which is considered to be the point indicative of a herd rebuilding phase. All four

quarters in 2021 had a female slaughter rate ranging from three to five percent below the corresponding quarter’s 10-year average (see Figure 1) and an annual average of 45 percent, indicating a strong turn towards building the size of the national herd.

Slaughter 2021

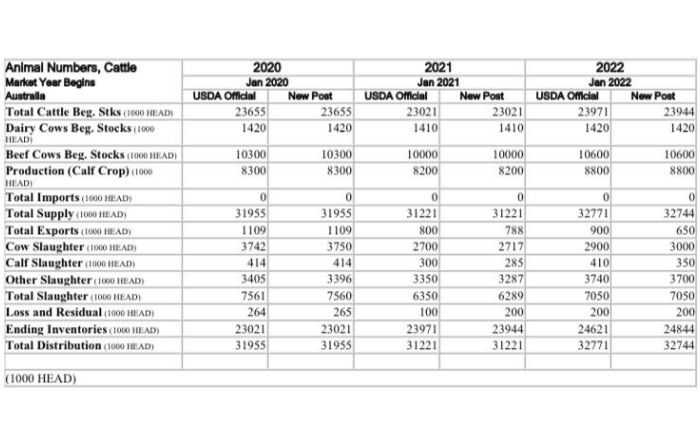

The FAS/Canberra forecast for cattle (calf crop) production in 2021 is unchanged and remains in line with the USDA official estimate.

Slaughter 2022

FAS/Canberra forecasts an increase in cattle slaughter in 2022 to 7.05 million head, a 761,000 head rise from 2021. The forecast 12 percent increase in slaughter numbers in 2022 is substantial considering the industry is in the early phase of the national herd rebuild. Although this is a large increase in forecast cattle slaughter, other than 2021 it still remains the lowest since 1984.

This forecast growth is led by the particularly good rainfalls across most of the beef cattle producing regions since the start of 2020. These conditions have enabled strong pasture growth over an extended period which has provided producers with the confidence to return to increasing the calf crop and at the same time increasing production of cattle for slaughter. However, the herd rebuild process has been a

little uneven, beginning in force in south-eastern Australia, but the recovery is a little further behind in the northern regions.

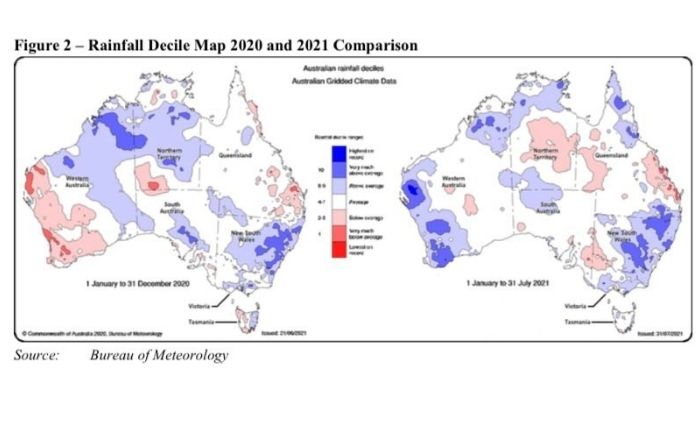

Since the start of 2020 the majority of Australian beef producing regions, particularly New South Wales, (which was hardest hit by the drought across 2018 and 2019), have had well above average rainfalls.

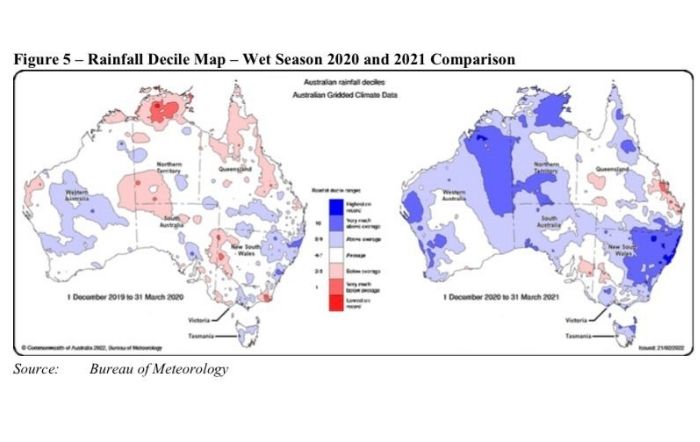

The rainfall results for these areas in 2020 would tend to indicate that pasture production should have been much better. However, these areas are mostly influenced by tropical wet season rains typically from December to March, during which the bulk of their pasture is produced. These wet season rains, along with some intermittent rains after the wet season, carry the feed requirement through to the end of the calendar year and prior to the commencement of the following wet season. The wet season period feeding into the 2020 pasture production (December 2019 to March 2020) in the northern tropical areas had below average rainfall compared to the subsequent wet season for 2021, which was generally average to above average (see Figure 5). This highlights the importance of the wet season rainfalls for annual pasture production in the northern tropical regions.

The current wet season period through to late February 2022 for the northern parts of Queensland and Northern Territory has been positive with generally average to above average rainfalls, which should support a continuation of the herd recovery and these regions’ contribution towards the growth in the national herd.

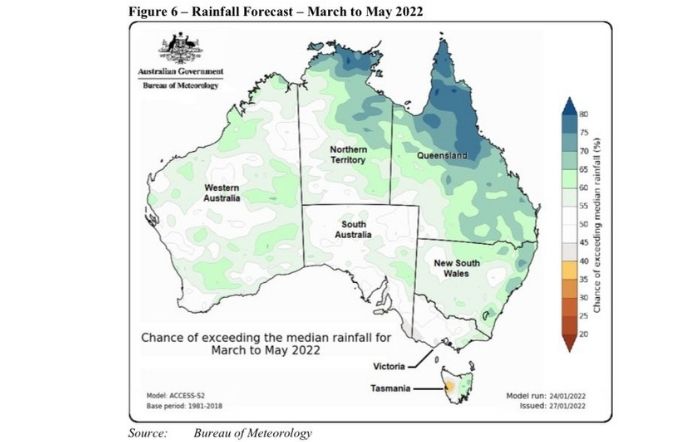

From a weather and pasture production perspective there are no looming concerns across the major beef cattle producing areas. The Bureau of Meteorology forecasts for rainfall during the March to May 2022 period is for a likelihood of average to above average rainfall (see Figure 6). This rainfall forecast provides further support for the expected continuation of the herd rebuild and improved cattle slaughter numbers in 2022.

2021

The cattle slaughter result for 2021 from the Australia Bureau of Statistics was 6.289 million head (including calves), merely 61,000 head below the USDA estimate of 6.35 million head, the lowest since 1971. A significant contributor to this variance was flooding rains across central and southern Queensland and northern New South Wales in late November 2021. This prevented transport access for

cattle to saleyards and also from feedlots to meat processors for around two weeks, which had a bearing on the final outcome.

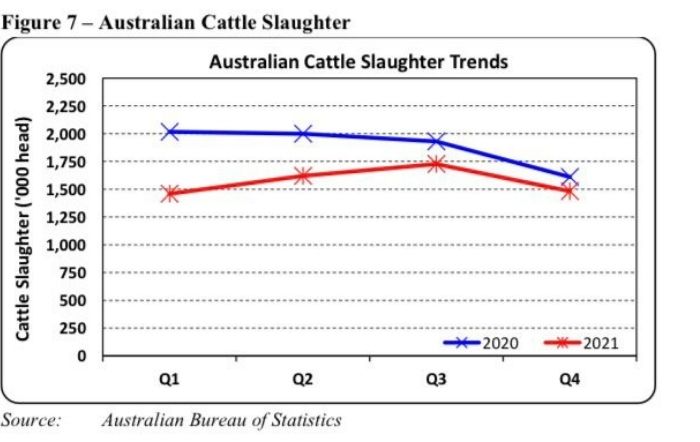

Interestingly, although the slaughter number in the first quarter of 2021 was some 558,000 head below that in 2020, the gap closed rapidly as the year progressed (see Figure 7). In the final quarter of 2021, there were only 129,000 head fewer slaughtered than in 2020, and if not for the flooding rains in late November 2021, the gap is expected to have been significantly narrower. The improving trend during 2021 augers well for the forecast higher slaughter number in 2022.

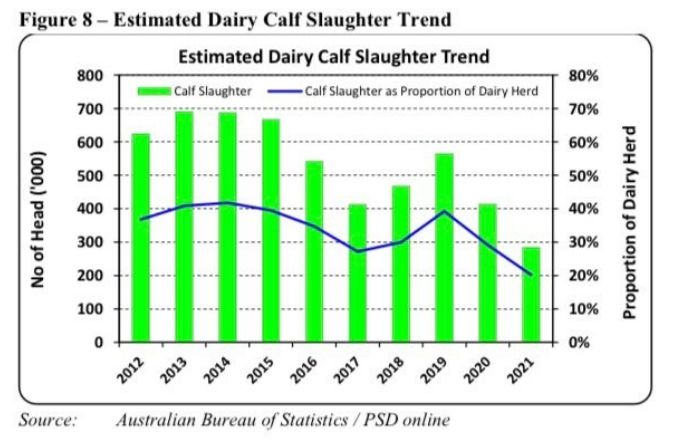

Of further interest is that the calf slaughter in 2021 was 285,000 head, by far at its lowest since records commenced in 1970. The majority of calf slaughter is from the dairy industry. With a dairy herd of 1.41 million head in 2021, a calf slaughter of around 20 percent is very low. Although calf slaughter has been a declining trend for well over a decade there was a significant drop in 2021 (see Figure 8). This is due to an increase in the number of dairy calves retained for meat production, due primarily to the record high beef cattle prices. With the expectation of beef cattle prices remaining high this trend of increased dairy calf rearing for meat production may continue.

Trade 2022

FAS/Canberra forecasts cattle exports in 2022 to decrease to 650,000 head, down 18 percent from 2021 and 250,000 head lower than the official USDA forecast. If realized this would be the lowest level since 2012. This large downward revision is in part driven by a shortage of available supply of stock suitable for the live trade and the current high cattle prices challenging the economic feasibility of Australia’s main export customers.

Industry sources indicate that available stock for the live trade were depleted in 2021 and, as mentioned earlier, the northern parts of Queensland and the Northern Territory (where most beef cattle for live export are sourced) are a little further behind in their herd rebuilding phase. This is limiting the available supply of livestock for the trade in 2022.

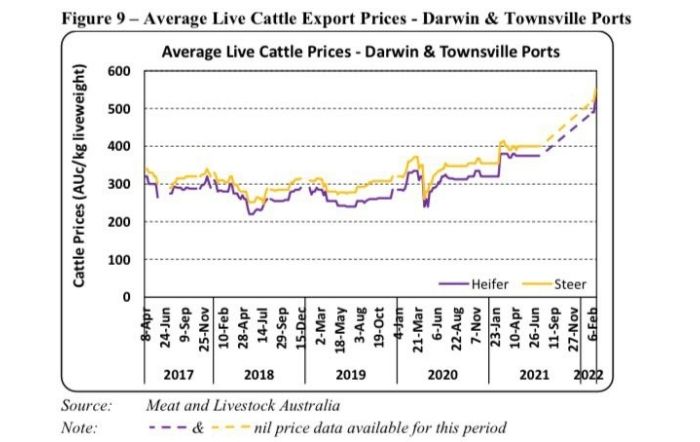

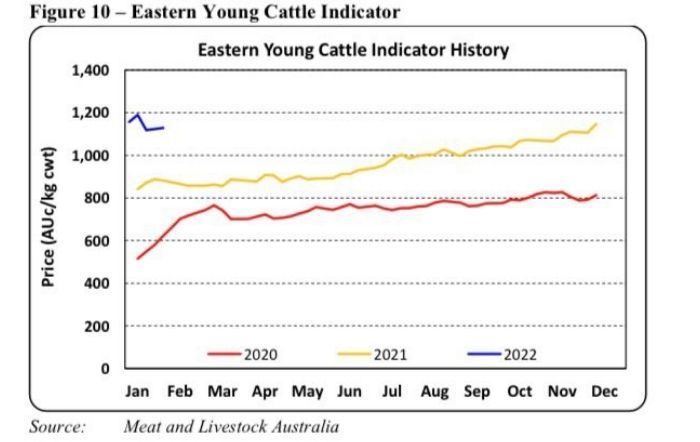

The price for live export cattle in early 2022 is around 25 percent higher from what were already considered high prices in the early months of 2021 (see Figure 9). These prices have been driven up by the demand from restockers and feedlots since early 2020, which has seen domestic cattle prices rise by well over 100 percent (see Figure 10) over the last two years and the Easter Young Cattle Indicator continuing to break records. Cattle producers in the more southern parts of northern Queensland and the Northern Territory typically have the option of supplying young cattle for live export or domestically. With such a steep rise in domestic prices it has drawn some of the available supply away from the live export market and also influenced the rise in live export prices.

Over recent years Indonesia has taken around half of all live cattle exports from Australia and almost all of them are destined for the feedlots there. Vietnam is the second largest market for live Australian cattle exports, averaging around 20 percent of the total over recent years. Vietnam sources mainly slaughterweight cattle from Australia, which typically go into their feedlots for only a short period. In feedlots, typically when cattle are kept for an extended period of time the high price of cattle at entry can be averaged down (on a cost per kilogram basis) if feed costs are low, enabling finished cattle to be sold at a lower unit cost (price per kilogram) than the original purchase price while still maintaining profitability in the feedlot. However, in Vietnam where the feedlot period is short, there is little scope to

average down the unit cost of the cattle with low feed costs. So, the live export market to Vietnam is very dependent upon the cattle purchase price and shipping costs.

In Indonesia, live cattle from Australia are typically in feedlots for around 100 days providing scope to average down the cost of the cattle with low-cost feed. However, it has been reported that food processors have been able to increase their extraction rates, leaving fewer and less nutritionally valuable byproducts for feedlots. With this, overall feed costs have also been increasing for Indonesian feedlots.

The combination of very high live cattle prices and elevated feed costs is expected to result in a significant decline in live cattle exports to Indonesia in 2022, from the already reduced level of 2021. With Australia in the early stages of a herd rebuild and at a point where cattle slaughter in 2022 is expected to be still at its second lowest on in nearly 40 years, there are no significant triggers anticipated in domestic circumstances that could result in a sharp decline in beef cattle prices. Combined with an expectation of ongoing strong world demand for beef during 2022, there looks to be little scope for any significant decline in live cattle export prices that could then drive any increased trade volumes of live cattle to the major destinations of Indonesia and Vietnam.

2021

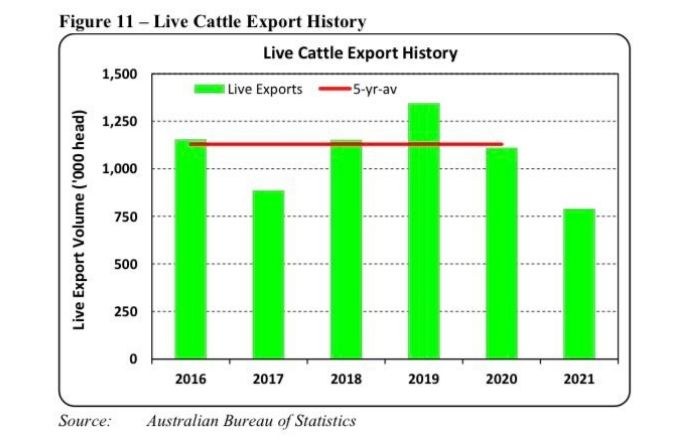

The live cattle export result for 2021 from the Australia Bureau of Statistics was 788,000 head, only 22,000 head below the official USDA estimate of 800,000 head. This is around 30 percent below both the previous 5-year average and the 2020 result (see Figure 11).

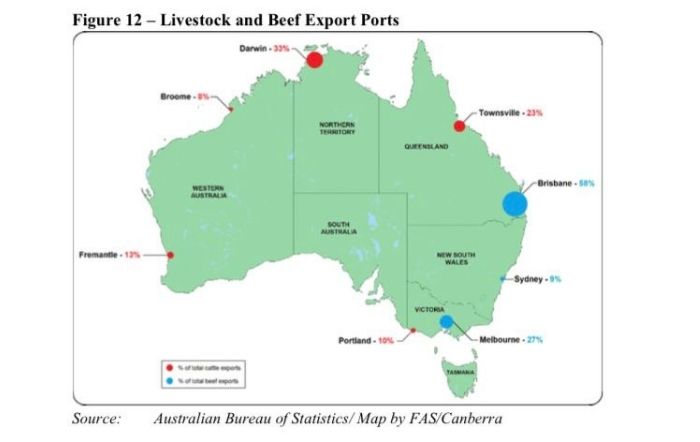

Most of the beef cattle sourced for the live export trade are from the northern part of the Northern Territory, north Queensland and Western Australia. These regions represent over three-quarters of all live cattle exports from Australia (see Figure 12). The other key live export port is Portland in Victoria which is more focused on the live dairy cattle trade due to its proximity to a major dairy farming region.

BEEF Production 2022

Beef production in 2022 is forecast to increase by 12 percent to 2.115 million metric tons (MMT) carcass weight equivalent (CWE) from the 2021 result of 1.888 MMT (CWE). This increase correlates with a forecast 12 percent increase in the cattle slaughter volume and slightly higher adult slaughter weights.

As previously mentioned, with much improved pasture production in 2021 and so far in 2022, grass-fed cattle carcass weights throughout 2022 should be above average and not have a negative impact on the overall average carcass weight. Further supporting the forecast marginal increase in average carcass weights is the expectation that there will be a slight increase in the proportion of Wagyu cattle

slaughtered from feedlots in 2022. Wagyu cattle are typically fed in feedlots for 400 days and slaughtered at around 400 kg CWE. With other adult cattle generally slaughtered at a little over 300 kg CWE, a slight increase in the proportion of Wagyu cattle slaughtered would have a small positive impact on the overall average slaughter weight for 2022.

There are, however, a number of negative factors that are constraining an even higher carcass weight. As mentioned earlier the calf slaughter result in 2021 was the lowest since at least 1970 and it is anticipated that in 2022 there will be a slight increase in the proportion of calf slaughter in the overall slaughter number, which will have downward impact on the overall average slaughter weight. A further

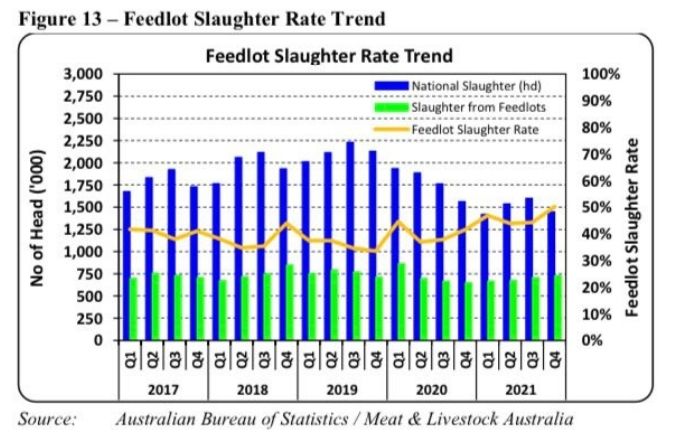

negative influence on the average slaughter weight in the forecast year is the expectation that the proportion of slaughter from feedlots will decline in 2022, after reaching a record high annual average of 46 percent in 2021 (see Figure 13). The overall number of cattle slaughtered from feedlots may increase in 2022 but the overall rise in grass-fed cattle slaughtered is expected to be even higher.

2021

Beef production for 2021 was 1.888 MMT (CWE) and less than one percent below the official USDA estimate of 1.9 MMT (CWE). As mentioned earlier there was substantial flooding in late November 2021 in central and southern Queensland and northern New South Wales which prevented cattle transport by road for around two weeks, negatively impacting the final result.

Consumption 2022

Domestic beef consumption is forecast to increase by eight percent to 665,000 MT (CWE) in 2022, from the upward revised 2021 estimate of 614,000 MT (CWE). This increase is related to the forecast rise in beef production and the lifting of COVID-19 related restrictions, particularly in the eastern states, including international travel. Relaxed international border polices are expected to boost the tourism sector, allow the arrival of international students, and boost inward migration which is anticipated to support retail and food service sector consumption despite the widening gap in beef prices to other meats.

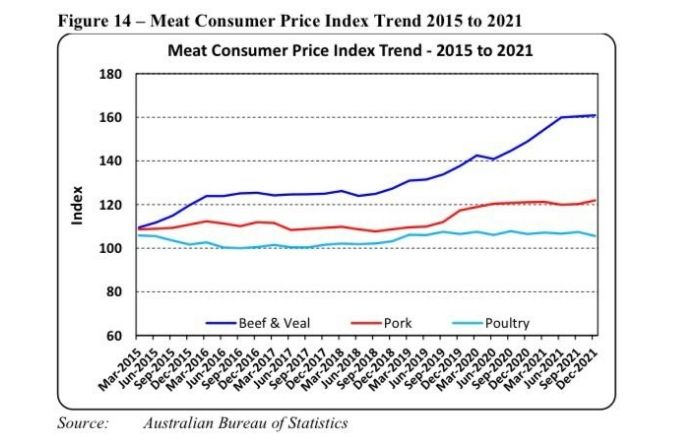

The increase in domestic beef cattle prices of well over 100 percent over the last two years, based on the Eastern young Cattle Indicator (see Figure 10), has filtered through to a substantial increase in the beef and veal consumer price index over the same period. This rise in beef prices is in contrast to lamb, pork and chicken, which have essentially remained stable (see Figure 14). Although beef consumption has declined somewhat in the recent COVID-19-impacted years, it remains robust considering the widening price differential to other meats.

2021

The FAS/Canberra beef consumption estimate for 2021 has been revised up to 614,000 MT (CWE) from the official USDA estimate of 605,000 MT (CWE). This a significant reduction from 667,000 MT (CWE) in 2020 and is due to continued strong export demand for limited supply, placing pressure on the domestic supply and resulting in higher prices of beef.

Trade 2022

FAS/Canberra forecasts beef exports in 2022 to rise to 1.47 MMT (CWE), up 172,000 MT (CWE) from the 2021 result of 1.298 MMT (CWE) and in line with the official USDA forecast. However, exports will still be far below the recent peaks of over 1.7 MMT (CWE) in 2014, 2015 and 2019. The forecast increase in beef exports mainly relates to the expected increase in beef production in 2022.

There has been a noticeable trend towards rising grain-fed beef production in the Australian cattle industry, with slaughter from feedlots comprising 50 percent of total slaughter in the October to December 2021 period (see Figure 13). The result for 2021 was a significant increase on past results and was solely due to a low supply of grass-fed cattle to meat processors, rather than any major increase in

feedlot throughput. For 2022, there is an expectation that grain-fed beef production will improve further but will represent a lower proportion of the overall kill due to increased grass-fed beef production. Despite the rapid increase in beef cattle prices over the last two years, feedlots have managed to pass on these higher costs as domestic consumers and consumers in key export markets develop an increasing preference for grain-fed beef.

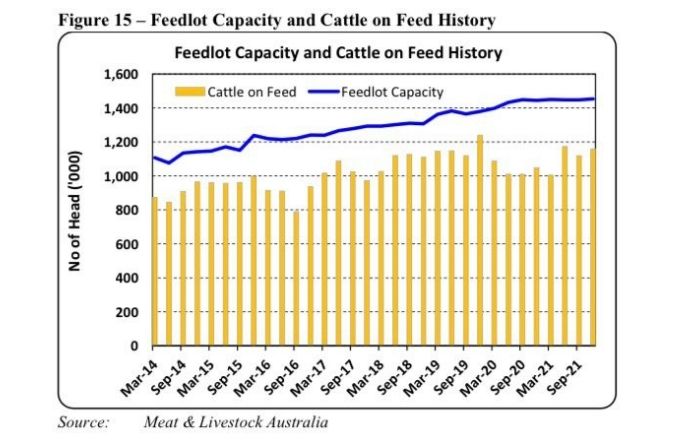

The feedlot industry has for some time had confidence in shifting consumer preference towards the higher value grain-fed beef, demonstrated by the expansion in feedlot capacity and increasing volume of grain-fed beef production. Over the last 5 years, feedlot capacity has increased by 17 percent and cattle on feed by 24 percent (see Figure 15). This general trend is not expected to abate in the short to medium term.

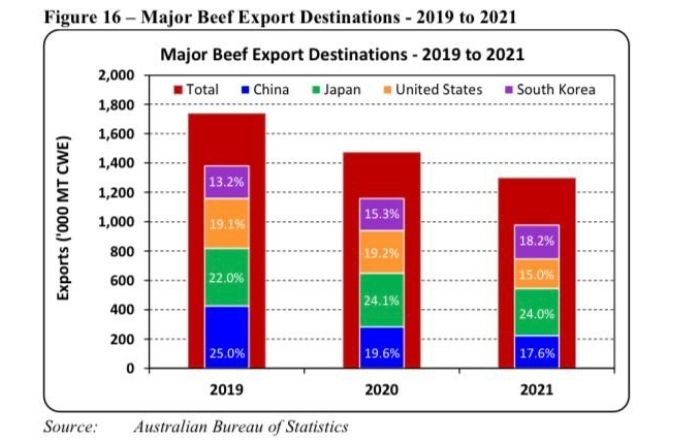

The four major export destinations for Australian beef – Japan, China, United States and South Korea – have in recent years accounted for 75 to 80 percent of Australian beef exports. Despite a decline in overall exports over the last two years, the proportion of beef exports to the four major destinations has remained stable (see Figure 16). With the forecast increase in beef exports for 2022 this is expected to

continue.

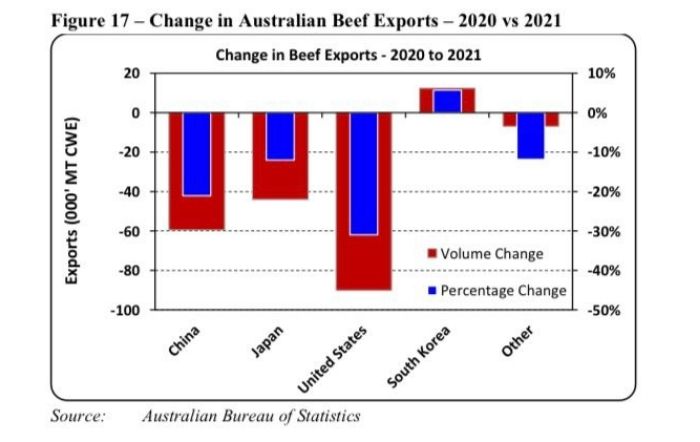

There has, however, been a shift in the balance of beef exports between the four major destinations. Despite an overall decrease in beef exports from 2020 to 2021, the volume of exports to South Korea increased by six percent and it went from being the fourth largest destination to the second largest destination behind Japan. Beef exports in 2021 to the United States, China, and Japan had all decreased

by 31 percent, 21 percent, and 12 percent, respectively (see Figure 17).

China had increased its overall imports of beef in 2021 but the decline in imports from Australia was driven by the low supply and high price of Australian beef. This encouraged Chinese traders to seek alternate supply with substantial increases in imports from Uruguay and the United States.

The majority of beef exports to the United States is lean grinding beef mainly from cows. With Australia entering a herd rebuild in 2021, there was a substantial reduction in beef production combined with the female slaughter rate dropping to 45 percent. As a result, it is unsurprising that the greatest decline in beef exports was to the United States. Over the last 10 years there appears to be a relatively strong

correlation between cow slaughter in Australia and beef exports to the United States (see Figure 18). With an increase in cow slaughter of around 10 percent forecast in 2022, a similar rise in beef exports to the United States in 2022 is possible.

PORK Production

FAS/Canberra forecasts Australia’s pork production in 2022 to reach a new record of 450,000 MT (CWE), up slightly from the 2021 record outcome of 444,000 MT (CWE). Domestic pork prices firmed in the second half of 2021 and following a second successive record winter crop production year, feed prices have remained far below the levels reached during the drought. With no major shift anticipated in

what are strong pork prices and with ample supply of feed grain at good prices conditions are set for a modest one percent growth in pork production

The impacts of African Swine Fever (ASF) on the global market are reported to be easing, particularly as the pig herd rebuild in China continues. However, a full recovery of the pig industry in China is expected to take some time and for this reason world pork prices are likely to remain firm in 2022. Even though Australia is not a significant exporter of pork, these world pork prices have an influence over

domestic prices and in turn sentiment towards production.

Consumption

Pork consumption is forecast to remain stable in 2022 at near peak levels, primarily due to the expectation of relatively stable production and trade. The consumer pork price index has increased only modestly over recent years, and poultry prices have had even less of an increase, whereas beef has seen a large and rapid rise. Interestingly, since 2015 beef consumption has declined by a little over 200,000 MT (CWE) while pork consumption has increased by merely 50,000 MT (CWE), and poultry has had the biggest rise at a little under 150,000 MT (CWE) The large rise in beef prices has resulted in consumers mainly substituting beef for chicken

rather than pork.

Consumption of pork in 2021 has been revised up to 616,000 MT (CWE) from the official USDA estimate of 605,000 MT (CWE), representing around a five percent increase to that of 2020. This is part of a steady increasing trend over the last 20 years with consumption growth of almost 50 percent.

FAS/Canberra forecasts Australia’s pork imports to remain at 210,000 MT (CWE) in 2022, and in line with the official USDA estimate. If realized this would again be the lowest result since 2016. This relatively low level of imports is a consequence of the increasing domestic production and high import prices for pork. Pork import prices have steadily risen over the last three years with the average annual price increasing by 23 percent since 2019 (see Figure 21). However, import prices declined over the tail end of 2021 and fell below the corresponding period in 2020.

Over recent years the top four suppliers of pork to Australia have accounted for over 90 percent of overall imports. The United States is the largest supplier, however its share decreased to 38 percent in 2021 from over 50 percent in the previous two years (see Figure 22). In 2021 the three other major suppliers – Netherlands, Denmark and Ireland – all substantially increased supply to Australia.

Pork imports in 2021 were 210,000 MT (CWE), 5,000 MT (CWE) higher than the official USDA estimate of 205,000 MT (CWE). This higher import result is despite production exceeding earlier expectations and was influenced by higher domestic consumption demand than previously anticipated.

Exports

FAS/Canberra forecasts exports in 2022 to remain stable at 40,000 MT (CWE), up 2,000 MT (CWE) from 2021 and in line with the official USDA forecast. Australia is a small exporter of pork and trades far less than it imports. With no change to production and imports forecast for 2022, there is also very little change forecasted for exports in 2022.

Australian pork exports are relatively low at around nine percent of production and over 90 percent is to seven countries in Asia. Singapore is the most important destination with around one-third of overall exports. In 2021 Papua New Guinea, New Zealand and the Philippines each accounted for 12 to 15 percent of overall exports. The Philippines and South Korea significantly increased as export

destinations while Vietnam and Hong Kong decreased. Pork exports for 2021 were at 38,000 MT (CWE).