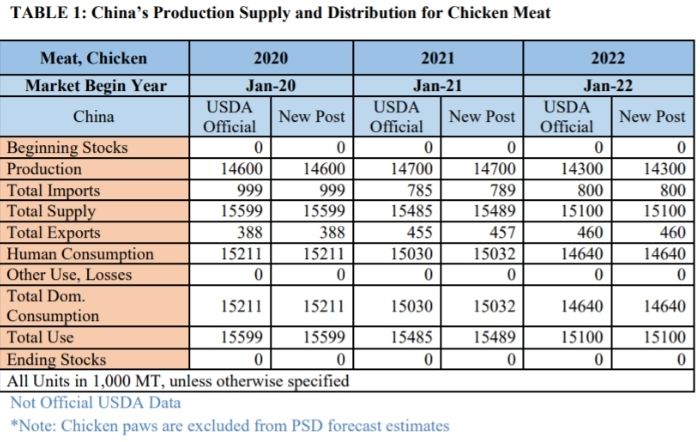

FAS China estimates for 2022 chicken meat align exactly with USDA Official estimates for production, supply, and distribution and only minor adjustments based on trade data are made for 2021.

Production:

In 2022, chicken meat production is forecast lower at 14.3 million MT (MMT), a 3 percent decrease from 2021. Chicken production only includes white feather broiler, yellow feather broiler, spent hens and hybrids. China’s government estimates for poultry production include fowl other than chicken. White broiler production is forecast to remain unchanged in 2022. However, chicken production will be

impacted by declines in yellow broiler production and producers leaving the market due to prolonged low chicken prices. The government has signaled that it expects poultry production, including fowl other than chicken, to decline to pre-2020 levels.

Consumption:

In 2022, chicken consumption is lowered to 14.6 MMT. Domestic consumption is forecast lower due to declines in consumption of yellow broiler products, a less optimistic economic outlook, and adverse effects on the hotel, restaurant, and institutional (HRI) sector stemming from government measures introduced to control COVID-19 outbreaks.

Imports:

In 2022, imports of chicken meat (excluding paw) are projected to reach 800,000 MT, an increase over 2021. Chicken paws are not included in the PSD estimates for imports of chicken. Domestic production is forecast to decline slightly making imports more attractive.

Exports:

China’s 2022 chicken meat exports are forecast to reach 460,000 MT, effectively flat compared to 2021, as Hong Kong and Japan continue to adapt to COVID-19 disruptions. Exports to other markets such as the Netherlands and ASEAN member countries as expected to remain stable.

Chicken meat production expected to decline, while white broiler to remain unchanged

China’s 2022 chicken meat production is forecast at 14.3 million metric tons (MMT), representing a 3 percent decline from 2021. Chicken meat production includes white feather broiler, yellow feather broiler, spent hens and hybrid chickens.1 China’s National Bureau of Statistics (NBS) and the Ministry of Agriculture and Rural Affairs (MARA) include a broader range of poultry in their poultry production

estimates.

Yellow broiler production is forecast to decline in 2022 as consumers move increasingly to online shopping or to modern retail channels to purchase chicken products. In these channels, yellow broiler products are expected to face pressure from lower priced white broiler chilled and frozen products.

Furthermore, closures of wet markets around China make yellow broiler purchases, as the fowl are typically marketed live or just after slaughter, increasingly difficult. White broiler production is expected to remain unchanged in 2022. In 2021, large producers profit

margins shrank due to low chicken prices, high capital investments, and high feed prices through the third quarter. In the first half of 2022, large scale producers are expected to continue to increase market share by accepting lower profit margins, effectively pushing smaller producers to exit the market. Industry sources indicate that large producers now account for nearly 70 percent of all white broiler

production.

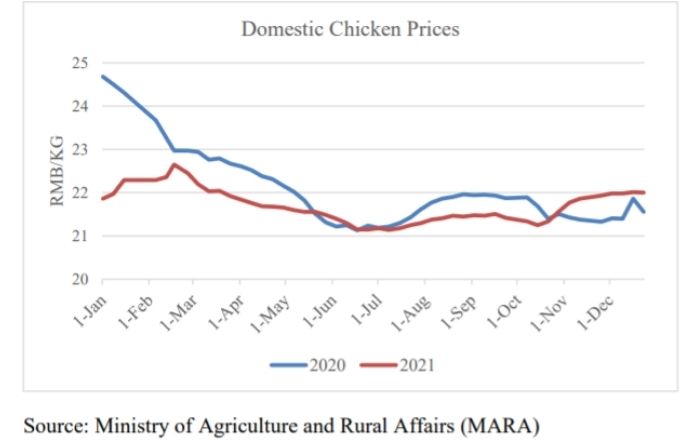

Figure 1: China: 2021 Domestic Chicken Prices Fall Below 2020 Through Q3

Over the last three years, large producers have expanded production facilities and diversified into feed, raising, slaughter, further processing and direct sales through retail and e-commerce platforms. In the second half of 2022, large-scale white broiler producers are expected to respond to higher poultry prices, which should be pulled higher alongside higher pork prices, by utilizing greater portions of production capacity. Smaller, less vertically integrated producers are expected to benefit from higher prices at that

time.

In 2022, layer production is estimated to increase as producers respond to higher egg prices, which have been on the rise since March 2021. Layer production has a longer time horizon than white or yellow broiler production, which means production gains are often delayed following increases in prices. For example, declining egg prices in 2020 led to a 1.7 percent decline in egg production in 2021 as reported by NBS.

Long road remains for commercialization of domestic white broiler genetics

In 2022, imported genetics are expected to remain the dominant source for China’s commercial white broiler operations. At the end of 2021, three new locally developed breeds of white broiler were approved by China’s National Livestock and Poultry Genetic Resources Committee for commercial production. According to industry contacts, for China to expand domestic breeding capabilities,

substantial investment, scale, and demonstratable results from these domestic breeds will be necessary.

Domestic Chicken Prices

A new breed of yellow broiler called “Huashan chicken” was approved for commercial production. Sources report the breed could be used in scaled-up production. However, some industry sources remain skeptical that extensive standardization of yellow broilers will be appealing to consumers.

China publishes announcement lowering poultry production estimates to pre-2020 levels Note: FAS China’s 14.3 MMT Chicken Production Estimate is only white and yellow broiler, spent hens, and hybrid chicken whereas the NBS and MARA data includes a broader range of poultry such as ducks and geese.

On December 2021, China’s MARA published the 14th 5-Year-Plan (2020-2025) for the Development of the National Animal Husbandry and Veterinary Industry. This plan indicates that poultry production should reach 22 MMT, lower than NBS data for poultry production in 2021, which reached 23.8 MMT. NBS poultry data includes a wide range of poultry products, a portion of which is chicken production.

This may be a signal from the government to encourage producers to lower poultry production. Sources indicate that poultry farms have been operating at a loss since late 2021 due to overproduction, high input costs, low pork prices, and weak consumer demand

Consumption trends in 2022

In 2022, chicken consumption is expected to decline 3 percent from 2021 to 14.6 MMT. Consumers in China often switch between pork and poultry depending on price, while pork remains the preferred meat. In 2021, pork prices declined and remained low through the end of the year and put downward pressure on chicken prices. Declines in yellow broiler consumption coupled with pork prices that are

anticipated to remain low through the first half of 2022, and a less optimistic general economic outlook for China will weigh on overall chicken consumption. White broiler consumption is expected to be flat in 2022. However, disruptions in food service, HRI and/or institutional channels from COVID-19 could negatively impact white broiler consumption.

White broiler trends

Consumer preferences are shifting from frozen to chilled (i.e., 0-4 C, with around 7 days of shelf life) white broiler products. Nearly 30 percent of domestically produced white broiler meat is sold chilled. However, the current limited availability of cold chain logistics constrains chilled white broiler products primarily to North China. In the long term, with large-scale investments, cold chain logistics may

expand the availability and support demand for chilled white broiler products across the country.

The consumption of fully or partially cooked processed chicken is expected to grow in the coming years. Processed chicken is mainly produced from white broiler meat, with a small share produced from hybrids and spent hens. Industry sources suggest that the catering industry will increase the use of fully or partially cooked chicken products to improve efficiency and profit margins. Retail consumers are also projected to gradually increase demand for new and innovative fully or partially cooked chicken products.

Yellow broiler trends

Consumers traditionally purchase fresh yellow broilers from wet markets, which are closing across China. Higher prices for yellow broilers, which get to market weight after a longer period, also make these products less competitive with white broiler meat at the retail level. These factors are expected to curb yellow broiler consumption in 2022. Furthermore, a less optimistic economic outlook for 2022 is

projected to negatively impact yellow broiler consumption in the HRI sector.

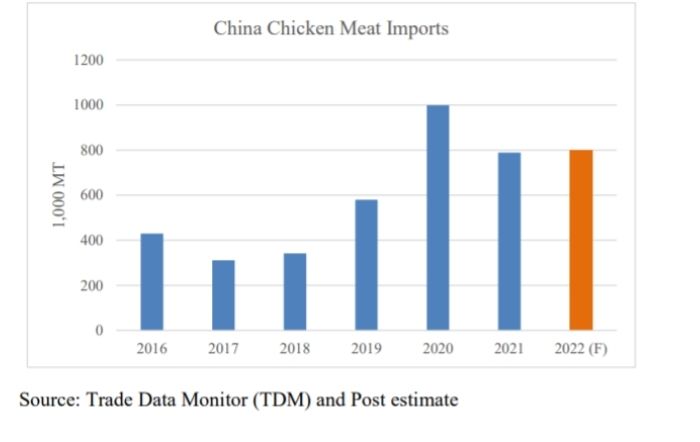

Chicken imports forecast to increase 2 percent to 800,000 MT in 2022

In 2022, chicken imports (excluding paw) are forecast to increase slightly from 2021 levels to 800,000 MT. In 2021, chicken imports declined due to lower domestic pork and chicken prices, supply chain disruptions, and China’s changing COVID-19 testing and disinfection measures for imported cold-chain products. Imports in 2022 are expected to improve over 2021(see Figure 2) as domestic chicken production tightens.

Figure 2: China: 2022 Chicken Imports Projected to Slightly Rise Over 2021

The United States and Brazil are expected to remain top chicken meat suppliers to China in 2022

The United States and Brazil are the top two chicken product suppliers to China. Brazil mainly exports chicken wings, legs, and paw. These three products have similar export volumes from Brazil. The United States also exports these products. However, U.S. chicken paw exports account for the majority of U.S. poultry export volume and value. U.S. chicken paw are not included in the PSD table.

GACC expands types of companies allowed to import meat In December 2021, GACC announced that starting on January 1, 2022, a consignee of imported meat will no longer be required in order to import meat products. This change provides an opportunity for a

range of new companies to import meat products. For example, large restaurants with multiple outlets, which were previously unable to import products directly from overseas may now apply to import meat products. This regulatory change is unlikely to impact the volume of imports but may increase the number of companies that import products directly and provide greater access to imported products for

the HRI sector.

China’s chicken exports in 2022

China’s 2022 chicken meat exports are effectively flat in comparison to 2021 as Hong Kong and Japan continue adjusting to COVID-19 disruptions. Hong Kong and Japan account for over 70 percent of China’s chicken meat exports. China’s chicken meat exports rose over 17 percent between 2020 and 2021, with growth across Hong Kong, Japan, the Netherlands and other ASEAN members.

For Japan, industry sources indicated that China’s producers are upgrading facilities to produce higher value-added products for Japanese convenience stores, such as individually packaged ready-to-eat products, rather than cooked chicken products for food service and retail channels. Similarly, these export-oriented processors have responded to health food trends in Japan by producing chicken products with fewer calories, less salt, and less sugar.

China’s exports to Hong Kong include fresh/chilled chicken and processed chicken products, which saw strong growth in 2021. Growth in China’s chicken meat exports to Hong Kong is expected to continue in 2022 as COVID-19 disruptions decline.

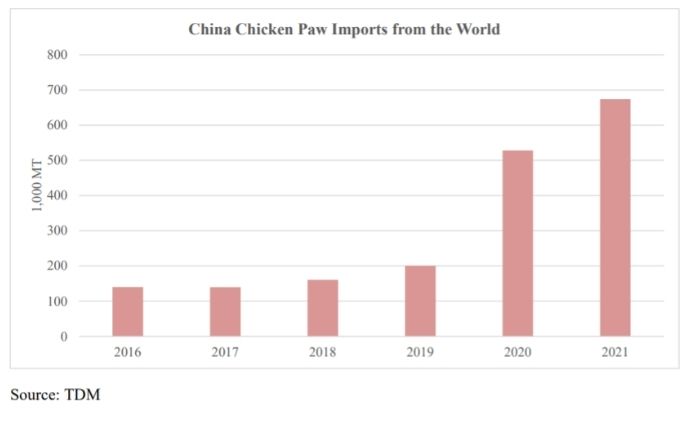

Chicken Paw

China’s chicken paw imports grew rapidly last year (see Figure 3) and the strong demand is expected to continue in 2022. The United States dominates China’s chicken paw import market with its unique “jumbo” paw. China’s imports from the United States dramatically increased in 2020, after the United States regained poultry market access in late 2019. In 2021, imports of chicken paw from the United

States grew by 44 percent year on year to 285,000 MT. Imports of chicken paw from the United States now account for over 40 percent of all chicken paw imports. Brazil is the second largest supplier of chicken paw, and its export volume grew 11 percent to 176,000 MT in 2021.

Figure 3: China’s Chicken Paw Imports

Turkey and Product Imports

In China, turkey and turkey cuts and related products are considered high-end and niche poultry products. In 2021, the U.S. became the top supplier of whole turkey and turkey cuts and related products to China. However, turkey remains a very small portion of China’s overall poultry imports accounting for less than 2 percent of all poultry imports. Promotional events and consumer education for turkey

products are encouraged and requested by various industry segments in order to build upon recent market successes.